As a small business owner you might need a small business loan to get you through a seasonal slow time, to fund a new product line, or to pay for equipment. While recording your loan and loan payments in QuickBooks Online isn't difficult, there are certain steps you will need to take in order to record everything accurately in your bookkeeping records. Let me show you how to record loan proceeds, payments, interest, and principal in your bookkeeping records. I will also be covering best practices for handling Shopify Capital Loans as well.

Our Loan Example

In our example, of how to record loans and loan payments, the loan amount is $10,000, the loan term is 24 months, and the interest rate is 3.5%. I input this information into the free to use loan calculator below in order to generate an amortization schedule. An amortization schedule lets you know how much each payment will be, and what amount of each payment is principal and what portion is interest. Your lender may provide you with an amortization schedule. Now that we have our amortization schedule, let's head to QuickBooks.

The Loan Calculator (Generate an Amortization Schedule)

Loan Accounts (Categories) in QuickBooks

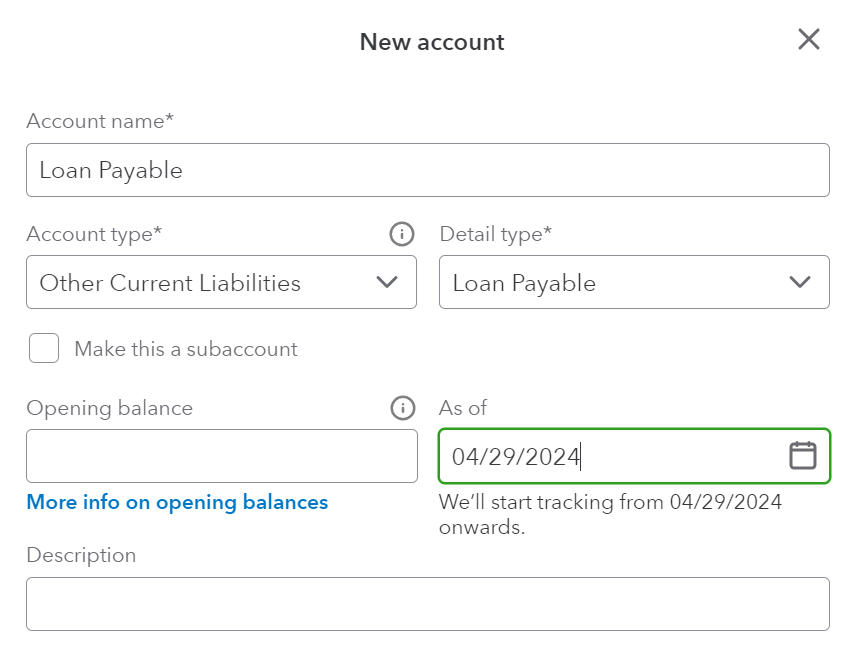

In QuickBooks we are first going to create the accounts that we need. On the left menu go to Transactions – Chart of Accounts, then select New. You will enter an Account Name then Account Type followed by a Detail Type. Create the following:

- Loan Payable – Other Current Liabilities – Loan Payable

- Interest Expense – Expense – Interest Paid

When creating the Loan Payable account, you should leave the Opening Balance field blank for our purposes.

Categorize the Loan from the Bank Feed

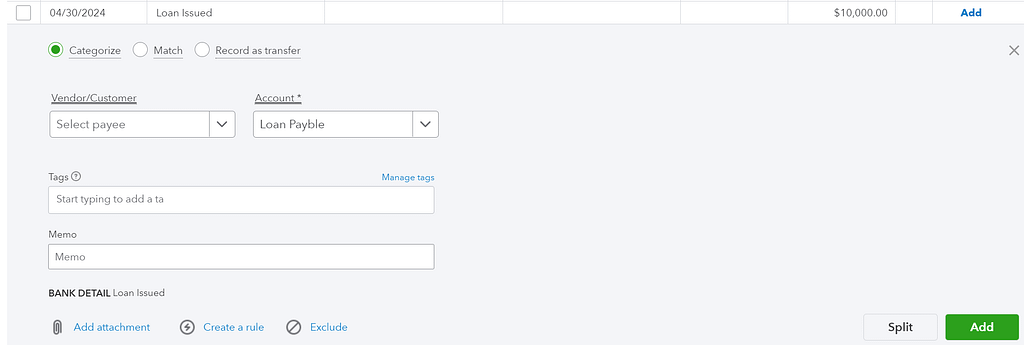

I have already linked my business bank account to my QuickBooks Online account, so when I go to Transactions, Bank Transactions, and then select my Checking account, I can see the deposit of the loan proceeds I received as well as my loan payments, as all have flowed through my business checking account.

In our first example, I received $10,000 in loan proceeds. It may be tempting to record this to an income account, but money you receive from a loan arrangement is a liability to you, money you will eventually have to pay back, so record the loan proceeds to the Loan Payable account we created.

Categorize your Monthly Loan Payments

Now let's record the first payment on the loan. From our loan amortization schedule we created, we know that each payment is $622.73. The first loan payment is comprised of $350 in interest, and $272.73 in principal. Each month, these amounts will change, and over time the amount of the payment that is interest will decrease, and the amount of the payment that is principal will increase. The principal amounts reduce the amount of the loan we still owe, while the interest portion is an expense to our business.

Each loan payment must be split into it's principal and interest components. When we select the first loan payment, we see a SPLIT button in the lower right corner of the box. This bring up the ability to choose multiple lines for our payment categorization. On the first line we will select Loan Payable as our category, and enter $272.73. On the second line we will choose Interest Expense as our category, and enter $350 as the amount.

Refer to your amortization schedule for each monthly payment. For example, next month you will enter $282.28 to Loan Payable and $340.45 to Interest Expense.

When you run your Balance Sheet report (or look at the Loan Payable register), you will see that the Loan Payable amount goes down with each payment, indicating that the amount you owe has been reduced. And when you run your Profit & Loss report you will see an Interest Expense amount each month. When your loan is finally paid off, the Loan Payable account on your Balance Sheet should be zero! I bet it feels good to have that loan paid off!

Record Shopify Capital Loan Payments

Now that you have mastered how to record standard loans and loan payments in QuickBooks Online. Another common loan scenario I see is Shopify Sellers, who take out a loan through Shopify Capital. This type of loan works a tad differently. Instead of monthly payments of the same amount, Shopify takes a portion of each sale as a loan payment. Because each sale amount could be of a different amount, the Shopify loan payments will also be different, and will not occur at regular intervals. Most likely the frequency of your loan payments will be greater than a typical loan structure.

While the general principals of accounting for a Shopify Capital loan and loan payments is the same, there is a little something I do differently due to the large volume of payments and varying transaction amounts. Rather than split each payment into it's principal and interest portion, throughout the period of the loan, I simply categorize the full amount of the payments directly to the Loan Payable. This means I'm not recording the interest expense during the life of the loan.

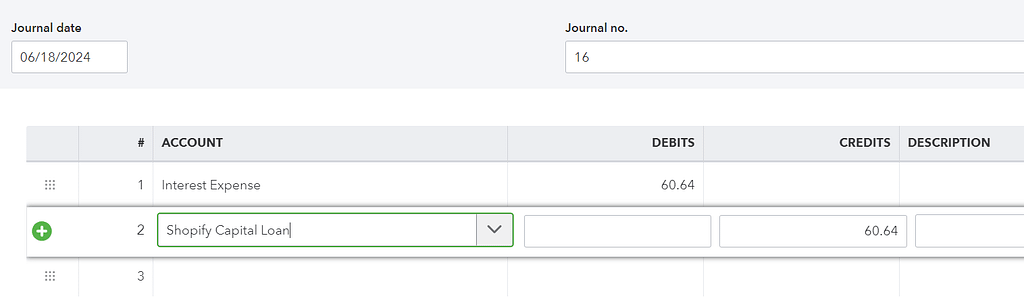

Shopify Capital loans tend to be of a shorter duration, and paid off much sooner than a typical loan. When the final Shopify Capital loan payment has been made, pull up your Balance Sheet (or the Shopify Capital Loan register). Your Shopify Capital Loan Payable account will be negative, so it appears as though we overpaid the loan. The “overpayment” is actually the interest expense, that we were not recording during the life of the loan.

To record the interest and get the Shopify Capital Loan Payable amount to zero, simply record a journal entry as of the date of the last loan payment. Your journal entry will Credit the Shopify Capital Loan Payable for the amount of the negative balance, and Debit Interest Expense, also for the amount of the negative balance. Now our Loan Payable will show as zero on the Balance Sheet (as it should) and our Interest Expense from the loan will also be recorded. Easy!

If your Shopify Capital loan straddles multiple years, determine what the ending balance should be as of December 31st, and post this same entry as above to record what interest expense you have paid for the year.

Any Questions?

Hopefully you have learned how to record loans and loan payments in QuickBooks Online. While it may not be difficult, there are a few special steps that need to be taken to ensure accurate bookkeeping records. It may not seem important at the time, but come tax time you will be glad you recorded everything correctly from the beginning. Any questions? Watch the video version of this tutorial and leave your question in the comments. I tend to answer almost every question asked of me on my YouTube channel.